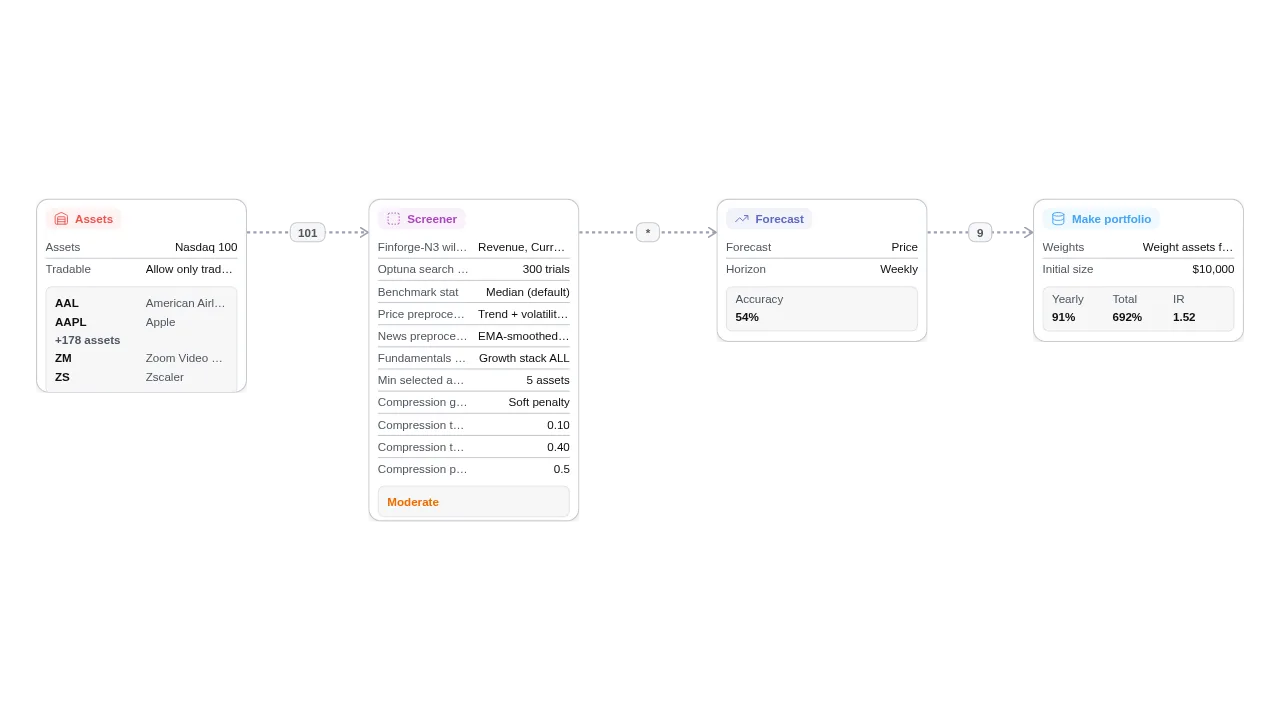

This template uses the datatype pair Revenue and Current Ratio. It runs a higher active-risk posture and historically exhibits larger benchmark-relative swings. This archetype is typically linked to elevated volatility, greater active dispersion, and deeper drawdown episodes compared with defensive or benchmark-hugging styles. In exchange for higher risk intensity, it targets stronger differentiation from the benchmark path.

Screener-N3 continually learns which combinations improve selection quality over time.

The screened assets are then passed into Forecast-N3, which estimates near-term return direction and magnitude.

Rather than applying another hard screen, the flow goes straight into portfolio construction, where stronger forecasts receive larger weights.

The result is a structure that keeps diversification from the screener while allowing the model to react more quickly through dynamic sizing.

That makes node chaining meaningful: screening reduces noise, forecasting adds timing, and portfolio construction turns both into actionable allocations.