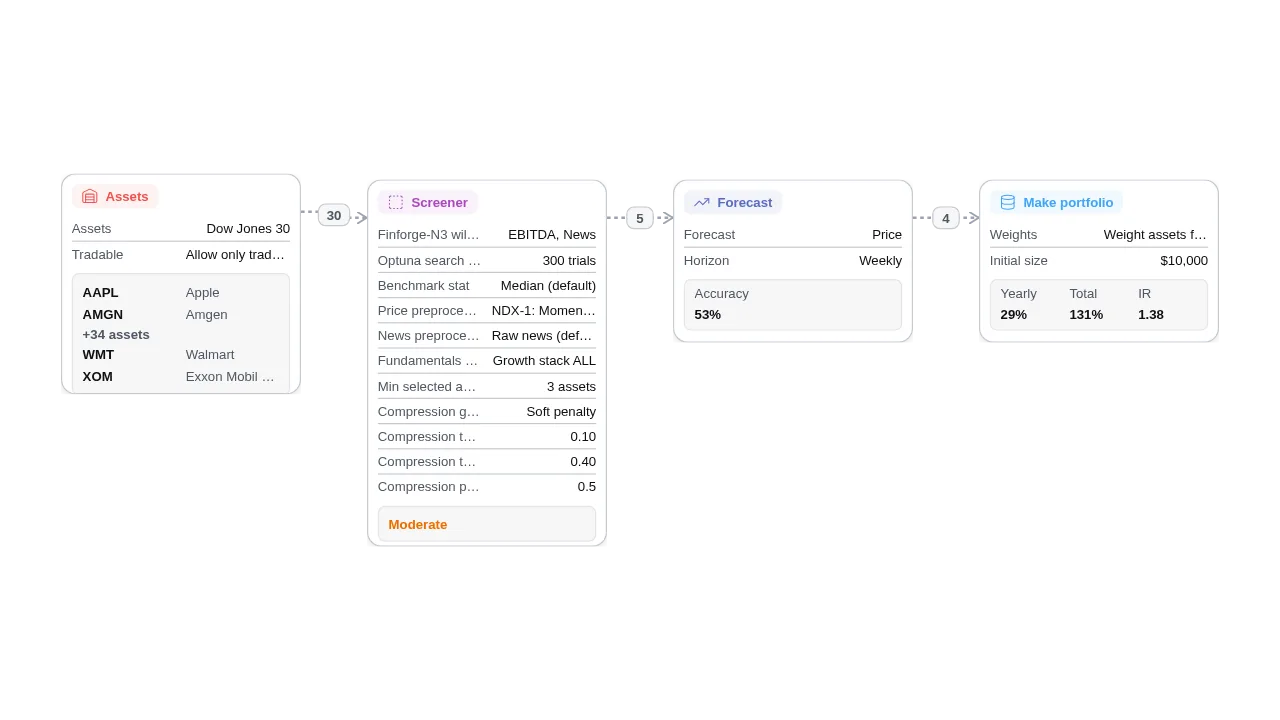

This template uses the datatype pair EBITDA and News. It updates portfolio composition more frequently and is structurally more responsive to changing signals. Historical behavior generally shows higher turnover dynamics, with faster transitions in holdings and style exposures than persistence-oriented profiles. This can improve adaptability in shifting markets, but it also means the portfolio identity can evolve more quickly through time.

Screener-N3 continually learns which combinations improve selection quality over time.

The screened assets are then passed into Forecast-N3, which estimates near-term return direction and magnitude.

Rather than applying another hard screen, the flow goes straight into portfolio construction, where stronger forecasts receive larger weights.

The result is a structure that keeps diversification from the screener while allowing the model to react more quickly through dynamic sizing.

That makes node chaining meaningful: screening reduces noise, forecasting adds timing, and portfolio construction turns both into actionable allocations.