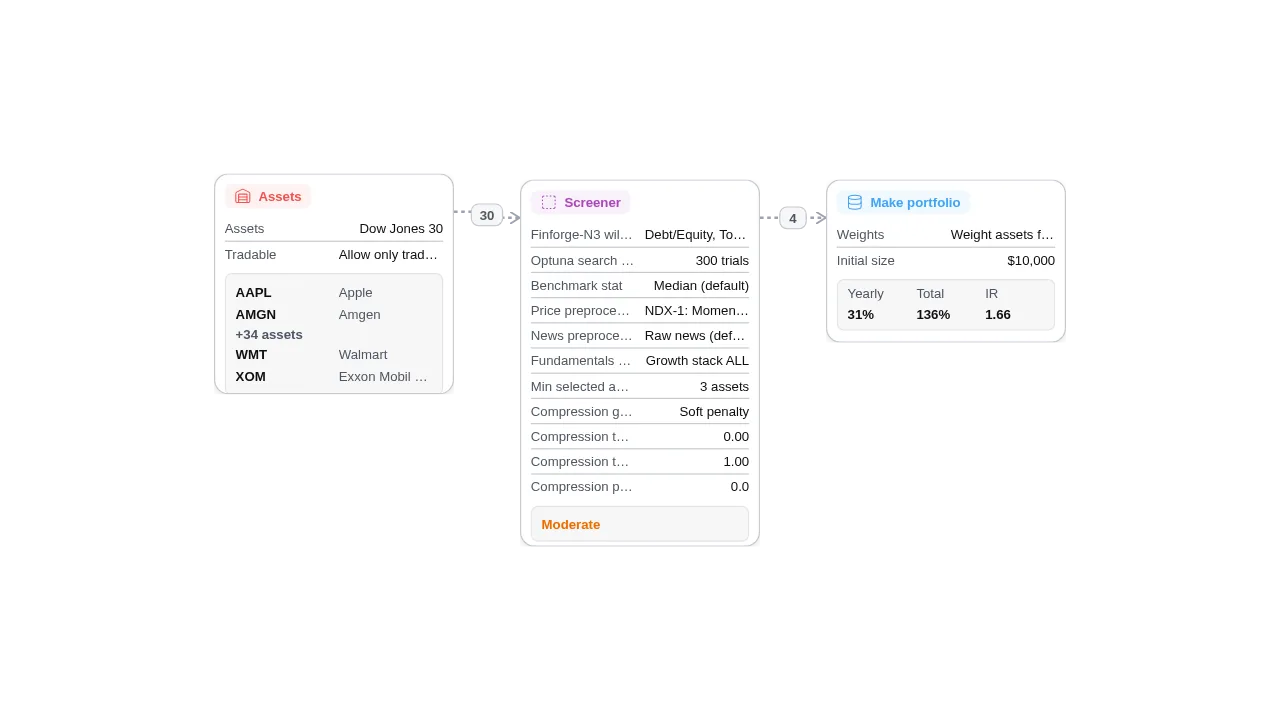

This template uses the datatype pair Debt/Equity and Total Assets. It is designed to stay relatively close to benchmark behavior instead of taking large benchmark-relative bets. In historical samples this profile usually appears with lower tracking error and a narrower range of benchmark-relative outcomes, so return paths tend to be steadier and more index-like. This style can still add value, but historically it has done so through incremental edge rather than extreme active dispersion.

Screener-N3 continually learns which combinations improve selection quality over time.

Because this variant does not include a forecast stage, the screened assets move directly into portfolio construction.

Portfolio construction assigns weights from screener conviction while respecting portfolio constraints.

The result is a simpler and more stable structure that prioritizes selection quality over short-term timing.

That makes node chaining meaningful: universe definition sets the opportunity set, screening reduces noise, and portfolio construction turns both into actionable allocations.